SBI FD and RD Interest Rates for 2026: Everything You Need to Know

India’s largest public sector bank, the State Bank of India (SBI), is offering interest rates of up to 6.45% on term deposits for the general public and up to 6.95% for senior citizens in 2026. These rates apply to both fixed deposits (FDs), where customers invest a lump sum, and recurring deposits (RDs), which allow savers to invest smaller amounts regularly over time.

Why SBI Revised Deposit Rates

SBI’s current deposit rates reflect changes in the broader interest rate environment. In 2025, the Reserve Bank of India (RBI) reduced the repo rate four times, cutting it by a total of 1.25 percentage points. Since the repo rate influences how cheaply banks can borrow money, these cuts prompted lenders to lower both lending and deposit rates to stay aligned with monetary policy.

The most recent revision came after the RBI cut the repo rate by 25 basis points in December, following which SBI updated its interest rates with effect from December 15, 2025.

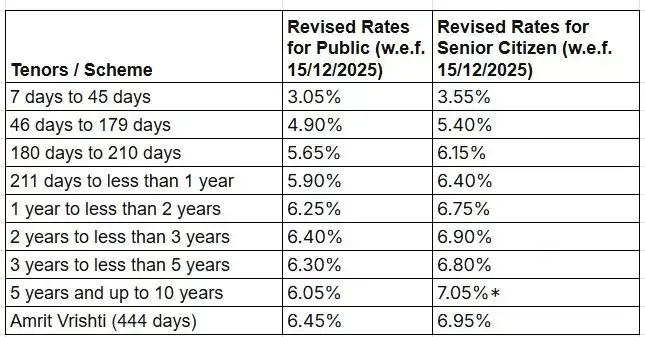

SBI Fixed Deposit And Recurring Deposit Rates In 2026

At present, SBI offers interest rates ranging from 3.05% to 6.45% on term deposits of up to ₹3 crore for general customers. Senior citizens are eligible for an additional 0.50%, which increases the maximum interest rate to 6.95%.

SBI has clarified that recurring deposits earn the same interest rates as fixed deposits for both general and senior citizens, making RDs an attractive option for those who prefer monthly savings over lump-sum investments.

Below are the interest rates applicable to term deposits under ₹3 crore as of December 15, 2025:

Extra Benefits For Super Senior Citizens

For customers aged above 80 years, SBI provides an additional interest benefit under the SBI Patrons scheme. However, this benefit is not applicable to certain deposit products, including recurring deposits, green rupee term deposits, the Tax Savings Scheme 2006, MODS, Capgain schemes, and non-callable term deposits.

Key Features Of SBI Recurring Deposits

SBI’s recurring deposit scheme is designed to encourage disciplined savings. The minimum deposit tenure is 12 months, while customers can choose tenures of up to 120 months. Deposits can start at just ₹100 per month, with increments of ₹10 allowed thereafter.

If a customer fails to pay six consecutive monthly instalments, the RD account is automatically closed and the available balance is paid out. SBI also levies penalties for delayed payments, highlighting the importance of timely contributions.

What Should Depositors Do Now?

With the RBI expected to keep a close watch on inflation and growth, further repo rate cuts cannot be ruled out. This could lead to another round of reductions in deposit interest rates. Customers looking for stable and predictable returns may consider comparing available FD and RD options and locking in current rates while they last.

For conservative investors seeking safety and reliability, SBI’s fixed and recurring deposits continue to remain a trusted choice in 2026, offering steady returns backed by the country’s largest lender.

Disclaimer: Readers are advised to verify the latest rates and details directly with SBI or through its official website before making any investment decisions. This article is for informational purposes only and should not be considered financial advice.

Why SBI Revised Deposit Rates

SBI’s current deposit rates reflect changes in the broader interest rate environment. In 2025, the Reserve Bank of India (RBI) reduced the repo rate four times, cutting it by a total of 1.25 percentage points. Since the repo rate influences how cheaply banks can borrow money, these cuts prompted lenders to lower both lending and deposit rates to stay aligned with monetary policy.

The most recent revision came after the RBI cut the repo rate by 25 basis points in December, following which SBI updated its interest rates with effect from December 15, 2025.

SBI Fixed Deposit And Recurring Deposit Rates In 2026

At present, SBI offers interest rates ranging from 3.05% to 6.45% on term deposits of up to ₹3 crore for general customers. Senior citizens are eligible for an additional 0.50%, which increases the maximum interest rate to 6.95%.

SBI has clarified that recurring deposits earn the same interest rates as fixed deposits for both general and senior citizens, making RDs an attractive option for those who prefer monthly savings over lump-sum investments.

Below are the interest rates applicable to term deposits under ₹3 crore as of December 15, 2025:

Extra Benefits For Super Senior Citizens

For customers aged above 80 years, SBI provides an additional interest benefit under the SBI Patrons scheme. However, this benefit is not applicable to certain deposit products, including recurring deposits, green rupee term deposits, the Tax Savings Scheme 2006, MODS, Capgain schemes, and non-callable term deposits.

Key Features Of SBI Recurring Deposits

SBI’s recurring deposit scheme is designed to encourage disciplined savings. The minimum deposit tenure is 12 months, while customers can choose tenures of up to 120 months. Deposits can start at just ₹100 per month, with increments of ₹10 allowed thereafter.

If a customer fails to pay six consecutive monthly instalments, the RD account is automatically closed and the available balance is paid out. SBI also levies penalties for delayed payments, highlighting the importance of timely contributions.

What Should Depositors Do Now?

With the RBI expected to keep a close watch on inflation and growth, further repo rate cuts cannot be ruled out. This could lead to another round of reductions in deposit interest rates. Customers looking for stable and predictable returns may consider comparing available FD and RD options and locking in current rates while they last.

For conservative investors seeking safety and reliability, SBI’s fixed and recurring deposits continue to remain a trusted choice in 2026, offering steady returns backed by the country’s largest lender.

Disclaimer: Readers are advised to verify the latest rates and details directly with SBI or through its official website before making any investment decisions. This article is for informational purposes only and should not be considered financial advice.

Next Story