EPFO clarifies who needs to file Form 121

Employees’ Provident Fund Organisation ( EPFO) has introduced a new compliance framework following the rollout of the Income-tax Act, 2025, clarifying who needs to file Form 121 instead of long-used Form 15G and Form 15H. The change has come into effect from April 1, 2026.

As per the EPFO circular issued on April 13, 2026, “With the phasing out of the old Income-tax Act, 1961, and the commencement of the Income-tax Act, 2025, effective from April 1, 2026, significant changes have been introduced regarding the declaration of income without deduction of tax. Under the new regulatory framework, the erstwhile Form 15G and Form 15H have been replaced by a single, consolidated written declaration in Form 121.”

Also read: EPFO extends facility to de-link wrong member IDs: Who should apply? Step-by-step process explained

Form 15G and 15H replaced with Form 121

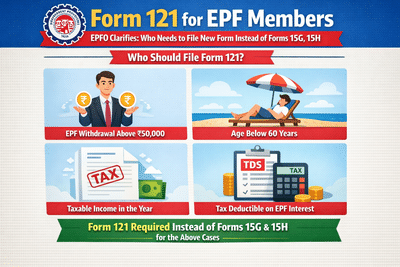

Taxpayers who previously used Form 15G (for individuals below 60 years) and Form 15H (for senior citizens) will now use a single unified declaration Form 121.

Note that this form is meant for taxpayers whose estimated total tax liability for the financial year is nil, allowing them to receive certain incomes without deduction of tax at source.

EPFO clarified that filing Form 121 is not mandatory for everyone. It is meant only for those who meet the eligibility conditions and wish to avoid TDS deductions.

Who should file Form 121?

Resident individuals (whether below 60 years or 60 years and above), Hindu Undivided Families (HUFs), and other specified eligible entities that meet the stipulated criteria should file it. The declarant, who is a resident, must ensure that their expected final tax liability for the year is nil and duly fill all the rows in Part A of the Form No121 and sign it.

Who is not eligible to file Form 121?

Companies and firms are not eligible to file Form 121. Non-residents are not eligible to file this form.

What is Form 121?

Form 121 is a self-declaration form submitted by taxpayers to confirm that their total income for the year will remain below the taxable limit. Once the form is submitted to the payer, such as EPFO, banks or financial institutions, TDS may not be deducted on eligible income.

Who will be issued a Unique Identification Number (UIN)?

The RO (as the payer) will allot a Unique Identification Number (UIN) to every Form 121 received. This UIN will include components such as a sequence number, the tax year, and the TAN of the payer.

Will claims submitted with Form 15G or 15H after April 1, 2026, be rejected?

The claims already filed along with Form 15G/H from April 1, 2026, will not be returned for this purpose, but Form 121 should be collected by taking up with the said member.

What does revised Form 121 consist of?

The revised Form No 121 will be a smart one to enhance user experience and providing the ease of filing through-

a. Auto-population/pre-filling of relevant details using information available from the profile.

b. Real time validations and error handling

c. Drop downs and date pickers

d. Integration with APIs and databases

e. Check box-based smart verification

f. Standardisation of name and address fields, etc.

As per the EPFO circular issued on April 13, 2026, “With the phasing out of the old Income-tax Act, 1961, and the commencement of the Income-tax Act, 2025, effective from April 1, 2026, significant changes have been introduced regarding the declaration of income without deduction of tax. Under the new regulatory framework, the erstwhile Form 15G and Form 15H have been replaced by a single, consolidated written declaration in Form 121.”

Also read: EPFO extends facility to de-link wrong member IDs: Who should apply? Step-by-step process explained

Form 15G and 15H replaced with Form 121

Taxpayers who previously used Form 15G (for individuals below 60 years) and Form 15H (for senior citizens) will now use a single unified declaration Form 121.

Note that this form is meant for taxpayers whose estimated total tax liability for the financial year is nil, allowing them to receive certain incomes without deduction of tax at source.

EPFO clarified that filing Form 121 is not mandatory for everyone. It is meant only for those who meet the eligibility conditions and wish to avoid TDS deductions.

Who should file Form 121?

Resident individuals (whether below 60 years or 60 years and above), Hindu Undivided Families (HUFs), and other specified eligible entities that meet the stipulated criteria should file it. The declarant, who is a resident, must ensure that their expected final tax liability for the year is nil and duly fill all the rows in Part A of the Form No121 and sign it.

Who is not eligible to file Form 121?

Companies and firms are not eligible to file Form 121. Non-residents are not eligible to file this form.

What is Form 121?

Form 121 is a self-declaration form submitted by taxpayers to confirm that their total income for the year will remain below the taxable limit. Once the form is submitted to the payer, such as EPFO, banks or financial institutions, TDS may not be deducted on eligible income.

Who will be issued a Unique Identification Number (UIN)?

The RO (as the payer) will allot a Unique Identification Number (UIN) to every Form 121 received. This UIN will include components such as a sequence number, the tax year, and the TAN of the payer.

Will claims submitted with Form 15G or 15H after April 1, 2026, be rejected?

The claims already filed along with Form 15G/H from April 1, 2026, will not be returned for this purpose, but Form 121 should be collected by taking up with the said member.

What does revised Form 121 consist of?

The revised Form No 121 will be a smart one to enhance user experience and providing the ease of filing through-

a. Auto-population/pre-filling of relevant details using information available from the profile.

b. Real time validations and error handling

c. Drop downs and date pickers

d. Integration with APIs and databases

f. Standardisation of name and address fields, etc.

Next Story