March 31, 2026 due date to file revised ITR?

Budget 2026 has changed the due date to file a revised Income Tax Return (ITR) to March 31 from the earlier December 31. But it is critical to note that this is applicable from assessment year 2026-27 and not assessment year 2025-26. In simple terms, March 31, 2026 is not the deadline to file revised ITR as this falls under AY 2025-26 (FY 2024-25).

So from next year onwards you can file revised ITR on or before March 31, 2027.

Revised Income Tax Return due date extended to March 31, 2026?

Chartered Accountant Avinash Rao, Partner at Mohindra & Associates, said to ET Wealth Online that the legislative intent was clearly not to extend this relief to AY 2025–26 (FY 2024–25). The Memorandum unambiguously provides that, though the amendment is effective from 1 March 2026, its applicability is prospective from AY 2026–27 onwards.

Rao says that it is equally important to note that the reference to 01.03.2026 also covers other amendments, including updated return provisions and the revised due date of 31st August, and cannot be read in isolation. Accordingly, a harmonious construction supports prospective applicability from AY 2026–27, though an explicit clarification or suitable proviso would be desirable to avoid unwarranted confusion or disputes.

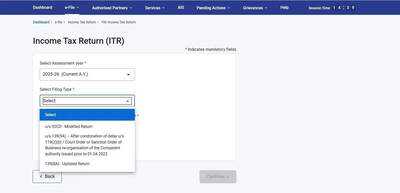

No option exists on the e-filing ITR portal yet

Chartered Accountant Ashish Niraj says to ET Weath Online that March 31, 2026 is not the due date to file revised ITR for AY 2025-26 and as such no such option exists on the e-filing ITR portal.

Niraj says that many experts are interpreting that since the Finance Bill 2026 has been notified, an income tax return that has already been filed can still be revised up to March 31, 2026 by availing the benefit of the amended provisions of Section 139(5) on payment of the prescribed additional fee. However till 2 PM on March 31, 2026, Income Tax Portal is not allowing ITR u/s 139(5) for AY 2025-26.

Niraj says: "Presently only 3 Filing Type coming for AY 2025-26 ,namely modified return u/s 92CD, u/s 139(9A) or Updated Return under section 139(8A)."

Who can file a revised ITR?

Who can file a revised ITR?

According to chartered accountant Abhishek Soni, co-founder, Tax2Win, taxpayers can file a revised Income Tax Return (ITR) to correct mistakes or omissions made in their original return. This is allowed under Section 139(5) of the Income Tax Act, 1961. Here are some of the most common reasons why someone might file a revised return:

According to KPMG, after Budget 2026 the due date for individuals / HUF filing income tax returns in Form ITR-1 and Form ITR-2 continues to be July 31, however, the due date would be extended to August 31, from July 31 for individuals and HUF having profits and gains from a business or profession, partners of a firm, and trusts whose accounts are not required to be audited.

The time limit for filing revised returns would increase to 12 months from 9 months from the end of the tax year (TY). However, a revised return filed after 9 months would attract a fee of Rs 1,000 (if total taxable income does not exceed Rs 5 lakh) or Rs 5,000 in all other cases.

So from next year onwards you can file revised ITR on or before March 31, 2027.

Revised Income Tax Return due date extended to March 31, 2026?

Chartered Accountant Avinash Rao, Partner at Mohindra & Associates, said to ET Wealth Online that the legislative intent was clearly not to extend this relief to AY 2025–26 (FY 2024–25). The Memorandum unambiguously provides that, though the amendment is effective from 1 March 2026, its applicability is prospective from AY 2026–27 onwards.

Rao says that it is equally important to note that the reference to 01.03.2026 also covers other amendments, including updated return provisions and the revised due date of 31st August, and cannot be read in isolation. Accordingly, a harmonious construction supports prospective applicability from AY 2026–27, though an explicit clarification or suitable proviso would be desirable to avoid unwarranted confusion or disputes.

No option exists on the e-filing ITR portal yet

Chartered Accountant Ashish Niraj says to ET Weath Online that March 31, 2026 is not the due date to file revised ITR for AY 2025-26 and as such no such option exists on the e-filing ITR portal.

Niraj says that many experts are interpreting that since the Finance Bill 2026 has been notified, an income tax return that has already been filed can still be revised up to March 31, 2026 by availing the benefit of the amended provisions of Section 139(5) on payment of the prescribed additional fee. However till 2 PM on March 31, 2026, Income Tax Portal is not allowing ITR u/s 139(5) for AY 2025-26.

Niraj says: "Presently only 3 Filing Type coming for AY 2025-26 ,namely modified return u/s 92CD, u/s 139(9A) or Updated Return under section 139(8A)."

According to chartered accountant Abhishek Soni, co-founder, Tax2Win, taxpayers can file a revised Income Tax Return (ITR) to correct mistakes or omissions made in their original return. This is allowed under Section 139(5) of the Income Tax Act, 1961. Here are some of the most common reasons why someone might file a revised return:

- Correction of Errors: If you realize that you have made an error or omission in your original ITR, such as reporting incorrect income while income tax filing, deductions, or any other information, you can file a revised ITR to correct those errors. This allows you to provide accurate and updated information to the tax authorities.

- Missed Reporting: If you inadvertently omitted certain income sources or failed to include certain deductions or exemptions in your original ITR, you can file a Revised Return to include those missed details. This helps ensure that your tax assessment is based on complete and accurate information.

- Changes in tax calculation: If there are changes in the tax laws, rules, or tax rates that affect your tax liability after you have filed your original ITR, you can file a Revised ITR to incorporate those changes in your tax calculation. This allows you to adjust your tax liability accordingly.

- Change in residential status: Shifting from resident to non-resident or vice versa after initial filing.

- Correction of assessment by tax department: Addressing discrepancies raised by the income tax authorities in their assessment.

- Claiming tax refund due: Realising you're eligible for a refund after the original filing due to overpaid taxes.

According to KPMG, after Budget 2026 the due date for individuals / HUF filing income tax returns in Form ITR-1 and Form ITR-2 continues to be July 31, however, the due date would be extended to August 31, from July 31 for individuals and HUF having profits and gains from a business or profession, partners of a firm, and trusts whose accounts are not required to be audited.

The time limit for filing revised returns would increase to 12 months from 9 months from the end of the tax year (TY). However, a revised return filed after 9 months would attract a fee of Rs 1,000 (if total taxable income does not exceed Rs 5 lakh) or Rs 5,000 in all other cases.

Next Story