PPF vs NPS: Which Investment Gives Higher Returns? Complete Guide

Planning for financial security after retirement has never been more important. With rising inflation, longer lifespans, and increasing expenses, choosing the right investment vehicle can make a significant difference in your post-retirement life. Among government-backed options, the Public Provident Fund (PPF) and the National Pension System ( NPS ) are two of the most popular schemes. While both aim to help you save and grow wealth for retirement, their features, risks, returns, and suitability differ. Let’s explore both in detail.

PPF: A Safe Haven for Conservative Investors

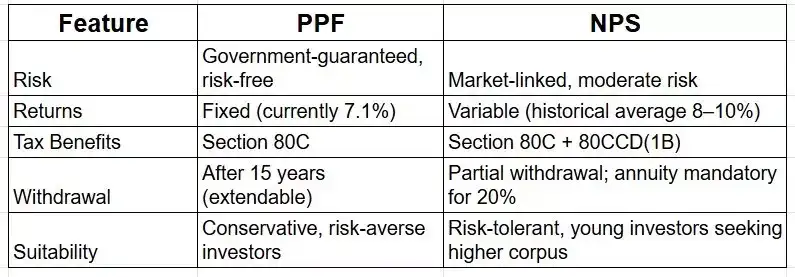

The Public Provident Fund is one of India’s oldest and most trusted investment schemes. Guaranteed by the government, it is considered risk-free, making it ideal for conservative investors who prioritize security and stable returns.

Interest Rate & Tenure: PPF currently offers an annual interest rate of 7.1%, fixed by the government each quarter. The initial tenure is 15 years, which can be extended in blocks of 5 years.

Investment Limits & Tax Benefits: Investors can deposit ₹500 to ₹1.5 lakh annually. One of the biggest advantages of PPF is its E-E-E feature: the principal, interest earned, and maturity amount are all completely tax-free. Contributions also qualify for a deduction under Section 80C, making it a tax-efficient long-term savings option.

Who Should Invest in PPF? PPF is suitable for risk-averse investors who prefer guaranteed returns, want tax-free growth, and aim to build a secure retirement fund. It is also ideal for long-term goals like children’s education, marriage planning, or emergency funds.

NPS: Market-Linked Growth with Pension Benefits

The National Pension System is a modern retirement scheme designed to help individuals build a sizable corpus over their working years. Unlike PPF, NPS is market-linked, investing in a combination of equity, corporate bonds, and government securities, which means it carries some market risk but offers higher potential returns.

Returns & Tenure: NPS returns are not fixed; they fluctuate depending on market performance. Historically, NPS has generated an average return of 8–10%. Investments continue until age 60, extendable to 70 for those who wish to continue contributing.

Investment Limits & Tax Benefits: While there is no maximum investment limit, tax benefits are capped at ₹1.5 lakh under Section 80C and an additional ₹50,000 under Section 80CCD(1B). This provides extra tax-saving opportunities for high-income investors.

Withdrawals & Risk: Upon retirement, 80% of the corpus can be withdrawn tax-free, while the remaining 20% must be used to purchase an annuity, providing a regular pension. Since it is market-linked, the corpus value may rise or fall with market conditions, making NPS a moderate to high-risk investment.

Who Should Invest in NPS? NPS is best for young investors with a long horizon who are willing to take moderate risks for higher returns. It is also suitable for those seeking a regular pension along with capital growth.

Which One Should You Choose?

Many investors also choose a hybrid approach, investing in both PPF and NPS. This combination provides the security of PPF with the growth potential of NPS, offering a balanced retirement portfolio.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Investments in NPS are market-linked and carry risk, while PPF is government-guaranteed. Individual financial goals and risk tolerance should be considered before investing. Always consult a certified financial advisor before making investment decisions.

PPF: A Safe Haven for Conservative Investors

The Public Provident Fund is one of India’s oldest and most trusted investment schemes. Guaranteed by the government, it is considered risk-free, making it ideal for conservative investors who prioritize security and stable returns. Interest Rate & Tenure: PPF currently offers an annual interest rate of 7.1%, fixed by the government each quarter. The initial tenure is 15 years, which can be extended in blocks of 5 years.

Investment Limits & Tax Benefits: Investors can deposit ₹500 to ₹1.5 lakh annually. One of the biggest advantages of PPF is its E-E-E feature: the principal, interest earned, and maturity amount are all completely tax-free. Contributions also qualify for a deduction under Section 80C, making it a tax-efficient long-term savings option.

Who Should Invest in PPF? PPF is suitable for risk-averse investors who prefer guaranteed returns, want tax-free growth, and aim to build a secure retirement fund. It is also ideal for long-term goals like children’s education, marriage planning, or emergency funds.

You may also like

- Centre provides security to Raghav Chadha after Punjab withdraws cover: Sources

- NHAI directs FASTag issuer banks to validate vehicle registration numbers

- NCW sets up panel to probe sex abuse allegations at TCS unit in Nashik

- Pakistan in dire straits as lenders ask for loan repayments

- Economic growth will be slower this quarter amid war, US Treasury chief says

NPS: Market-Linked Growth with Pension Benefits

The National Pension System is a modern retirement scheme designed to help individuals build a sizable corpus over their working years. Unlike PPF, NPS is market-linked, investing in a combination of equity, corporate bonds, and government securities, which means it carries some market risk but offers higher potential returns. Returns & Tenure: NPS returns are not fixed; they fluctuate depending on market performance. Historically, NPS has generated an average return of 8–10%. Investments continue until age 60, extendable to 70 for those who wish to continue contributing.

Investment Limits & Tax Benefits: While there is no maximum investment limit, tax benefits are capped at ₹1.5 lakh under Section 80C and an additional ₹50,000 under Section 80CCD(1B). This provides extra tax-saving opportunities for high-income investors.

Withdrawals & Risk: Upon retirement, 80% of the corpus can be withdrawn tax-free, while the remaining 20% must be used to purchase an annuity, providing a regular pension. Since it is market-linked, the corpus value may rise or fall with market conditions, making NPS a moderate to high-risk investment.

Who Should Invest in NPS? NPS is best for young investors with a long horizon who are willing to take moderate risks for higher returns. It is also suitable for those seeking a regular pension along with capital growth.

Key Differences Between PPF and NPS

Which One Should You Choose?

- PPF is ideal if you want safe, guaranteed, and tax-free returns with long-term planning in mind.

- NPS is suitable if you are comfortable with market risks, want higher returns, and aim for both a retirement corpus and a regular pension.

Many investors also choose a hybrid approach, investing in both PPF and NPS. This combination provides the security of PPF with the growth potential of NPS, offering a balanced retirement portfolio.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Investments in NPS are market-linked and carry risk, while PPF is government-guaranteed. Individual financial goals and risk tolerance should be considered before investing. Always consult a certified financial advisor before making investment decisions.

More from our partners

Loving Newspoint? Download the app now