Tax treaty relief may not come easy to Indian investors in UAE

As tensions from the Iran-Israel conflict cast uncertainty over West Asia, Indian investors operating out of Dubai are facing a parallel challenge from a landmark ruling by the Supreme Court of India. Tax experts say the judgment in the Tiger Global-Flipkart tax case may narrow the scope of treaty relief that many high-net-worth individuals and family offices rely on when structuring cross-border investments.

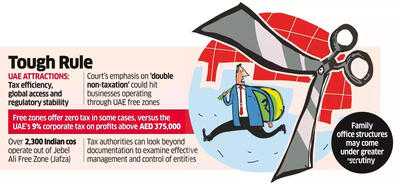

The decision has triggered fresh concerns among Indian HNIs, family offices, and companies that moved to the UAE or created free-zone entities for tax efficiency. Tax advisers are cautioning clients that treaty relief may no longer hinge on formal residency alone.

In January, the apex court held that capital gains arising from the US private equity major's $1.6-billion exit from Flipkart were taxable in India, denying benefits under the India-Mauritius Double Taxation Avoidance Agreement (DTAA) despite the presence of a valid tax residency certificate.

While the ruling arose under the Mauritius treaty, experts say its reasoning, "liable to tax", commercial substance and effective management, could have wider implications for the India-UAE tax treaty. Tax professionals say the judgment makes it clear that a residency certificate may now be treated as a necessary but not sufficient condition to claim treaty benefits. "This has direct implications for the India-UAE DTAA," said Ajay Rotti, founder of Tax Compaas. The court observed that for a treaty to be applicable, the claimant must prove taxability in the other contracting state. "This reasoning becomes particularly significant in the UAE context, where historically individuals were subject to little or no personal income tax," Rotti said. "The burden is clearly on taxpayers to demonstrate substantive fiscal residence rather than relying solely on residency certificates."

The court's observations on "double non-taxation" could also affect businesses operating through UAE free zones, which continue to offer zero tax in certain cases, compared with the UAE's 9% corporate tax on taxable profits exceeding AED 375,000. Tax authorities, advisers say, can now look beyond documentation to examine where the "head and brain", or effective management and control, of an entity is located, and whether there is real commercial substance in the claimed jurisdiction of residence.

Indian individuals, entrepreneurs, and family offices have been moving to Dubai and Abu Dhabi, drawn by tax efficiency, global access and regulatory stability, while often retaining core business operations and decision-making links with India. While the current regional uncertainty and war may act as a short-term deterrent, the lure and optimism remain, say tax advisers.

According to estimates by Henley & Partners, about 5,100 Indian millionaires left the country in 2023, followed by 4,300 in 2024 and around 3,500 in 2025, with the UAE emerging as a leading destination. Tax advisers warn that certain cross-border structures could now face closer examination. "Gulf structures could get affected, given the migration of Indian high-net-worth individuals and businesses to Dubai for lower or nil taxation," said Ashish Karundia, founder of CA firm Ashish Karundia & Co.

He pointed to arrangements where a Dubai entity is interposed between overseas suppliers and an Indian operating company without a clear commercial rationale. Under India's Place of Effective Management framework, a Dubai-incorporated entity can be treated as an Indian tax resident if it is effectively managed from India.

If a company routes imports from the US to India through a Dubai entity and parks profits there, such structures, if they are unable to prove commercial substance, could come under the scanner. "Genuine commercial setups should withstand scrutiny, but entities created solely for tax benefits are more likely to face challenges," he said.

Akhilesh Ranjan, a former member of the Central Board of Direct Taxes, said family office structures may come under greater scrutiny.

"The judgment has certainly created disruption," he said. "Family offices manage large pools of capital but often operate with minimal staff and rely heavily on consultants. If such entities invest in India and primarily exist in a low-tax jurisdiction without sufficient commercial rationale, treaty benefits on investment income could potentially be questioned."

He added that family offices would need a credible commercial reason for being located in jurisdictions such as the UAE, along with adequate operational substance.

Rajat Mohan, senior partner at AMRG & Associates, said advisers are already cautioning clients planning to shift assets to the UAE.

"Treaty claims can be challenged if management is effectively in India, investment decisions are taken in India, entities lack economic presence, or the structure is predominantly tax-driven," he said.

The decision has triggered fresh concerns among Indian HNIs, family offices, and companies that moved to the UAE or created free-zone entities for tax efficiency. Tax advisers are cautioning clients that treaty relief may no longer hinge on formal residency alone.

In January, the apex court held that capital gains arising from the US private equity major's $1.6-billion exit from Flipkart were taxable in India, denying benefits under the India-Mauritius Double Taxation Avoidance Agreement (DTAA) despite the presence of a valid tax residency certificate.

While the ruling arose under the Mauritius treaty, experts say its reasoning, "liable to tax", commercial substance and effective management, could have wider implications for the India-UAE tax treaty. Tax professionals say the judgment makes it clear that a residency certificate may now be treated as a necessary but not sufficient condition to claim treaty benefits. "This has direct implications for the India-UAE DTAA," said Ajay Rotti, founder of Tax Compaas. The court observed that for a treaty to be applicable, the claimant must prove taxability in the other contracting state. "This reasoning becomes particularly significant in the UAE context, where historically individuals were subject to little or no personal income tax," Rotti said. "The burden is clearly on taxpayers to demonstrate substantive fiscal residence rather than relying solely on residency certificates."

The court's observations on "double non-taxation" could also affect businesses operating through UAE free zones, which continue to offer zero tax in certain cases, compared with the UAE's 9% corporate tax on taxable profits exceeding AED 375,000. Tax authorities, advisers say, can now look beyond documentation to examine where the "head and brain", or effective management and control, of an entity is located, and whether there is real commercial substance in the claimed jurisdiction of residence.

Indian individuals, entrepreneurs, and family offices have been moving to Dubai and Abu Dhabi, drawn by tax efficiency, global access and regulatory stability, while often retaining core business operations and decision-making links with India. While the current regional uncertainty and war may act as a short-term deterrent, the lure and optimism remain, say tax advisers.

According to estimates by Henley & Partners, about 5,100 Indian millionaires left the country in 2023, followed by 4,300 in 2024 and around 3,500 in 2025, with the UAE emerging as a leading destination. Tax advisers warn that certain cross-border structures could now face closer examination. "Gulf structures could get affected, given the migration of Indian high-net-worth individuals and businesses to Dubai for lower or nil taxation," said Ashish Karundia, founder of CA firm Ashish Karundia & Co.

He pointed to arrangements where a Dubai entity is interposed between overseas suppliers and an Indian operating company without a clear commercial rationale. Under India's Place of Effective Management framework, a Dubai-incorporated entity can be treated as an Indian tax resident if it is effectively managed from India.

If a company routes imports from the US to India through a Dubai entity and parks profits there, such structures, if they are unable to prove commercial substance, could come under the scanner. "Genuine commercial setups should withstand scrutiny, but entities created solely for tax benefits are more likely to face challenges," he said.

Akhilesh Ranjan, a former member of the Central Board of Direct Taxes, said family office structures may come under greater scrutiny.

"The judgment has certainly created disruption," he said. "Family offices manage large pools of capital but often operate with minimal staff and rely heavily on consultants. If such entities invest in India and primarily exist in a low-tax jurisdiction without sufficient commercial rationale, treaty benefits on investment income could potentially be questioned."

He added that family offices would need a credible commercial reason for being located in jurisdictions such as the UAE, along with adequate operational substance.

Rajat Mohan, senior partner at AMRG & Associates, said advisers are already cautioning clients planning to shift assets to the UAE.

"Treaty claims can be challenged if management is effectively in India, investment decisions are taken in India, entities lack economic presence, or the structure is predominantly tax-driven," he said.

Next Story