Modular health plans: Benefits and risks explained

In the fast-evolving health insurance space, a significant shift is underway. Since the pandemic, the one-size-fits-all health plans have been giving way to customised or modular policies, wherein customers can choose benefits based on their needs, budgets, life stages and health conditions. The rising adoption of tailored coverage has been necessitated by increased lifestyle diseases and high medical inflation of 12-14%. “It’s also driven in large part by the Insurance and Regulatory Development Authority of India’s (IRDAI) 2024 Master Circular, which explicitly required insurers to offer add-ons and riders catering to diverse individual needs,” says Siddharth Singhal, Head of Health Insurance, Policybazaar.

What are modular plans?

A health plan consists of a base plan and riders or add-ons. Earlier, the base plan comprised fixed features that could not be changed, and one could add only 2-3 riders—usually critical illness, personal accident, co-pay/ deductible—at the time of purchasing the policy.

Over the past few years, the fixed base plan profile has altered and the number of optional features has increased to 15-25, each available at a price. These vary by insurers and can include a range of benefits, such as maternity, restoration of cover, reduced waiting periods for specific illnesses, inclusion of consumables, enhanced covers, hospitalisation daily cash, out-patient department (OPD) expenses and loyalty bonus, among several others.

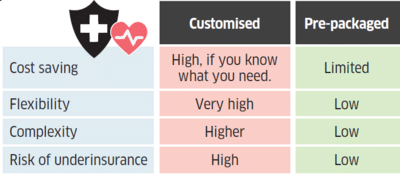

Pre-packaged plans offer a solid base with a handful of riders; useful, but limited in scope. Modular plans flip this: a leaner base, and a far deeper optional layer. While pre-packaged plans are still available, more and more insurers are moving towards modular products.

Most insurers typically have a flagship modular plan that is highly customisable, while other plans in their portfolios are standard, with fewer customisable options. For instance, ICICI Lombard General Insurance has a modular flagship plan, Elevate, while others are being reworked. “The modular chassis has been built for the next generation retail product, Elevate, but the same approach has been applied to multiple product lines for the future, while the older, existing plans have been restocked by adding riders and add-ons,” says Priya Deshmukh, Head of Health Products, Operations & Services, ICICI Lombard General Insurance.

Most insurers keep basic features, such as in-patient, domiciliary, AYUSH (ayurveda, yoga and naturopathy, unani, siddha, and homoeopathy), and pre- and post-hospitalisations in the base plan, while specialised, ailment- or segment-specific and cost-saving features are kept as addons. “For instance, while there is a base plan that caters to family, there are womencentric covers that can be tagged to the plan as add-ons,” says Santosh Puri, Head, Retail, Underwriting, TATA AIG General Insurance.

“The practical goal is to plug the gaps a standard plan leaves, whether it’s outpatient expenses, consumables, or maternity costs, without paying for coverage that isn’t relevant,” says Singhal.

There are plenty of financial lures in both the base and optional features, such as enhanced covers, loyalty bonuses, reduction of waiting periods, etc. Take ICICI Lombard’s Elevate, which offers add-ons like Infinite Care, a one-time infinite claim; Power Booster, a cumulative loyalty bonus of 100% of the expiring or renewed annual sum insured, whichever is lower; Jumpstart, which reduces waiting period to 30 days for certain conditions; Claim Protector, for non-payables; and Inflation Protector to protect against inflation, among others.

Similarly, ReAssure 3.0 from Niva Bupa Health Insurance offers add-ons like Cash Bag+ (cashback on every claim-free year, among several other options); Niva Bupa One (exclusive membership); hospital daily cash; pre-existing disease wait time modification to 1-2 years; Wellconsult+ (up to five times the total premium for OPD coverage), among 43 such features.

Other insurers have tried to flip the pattern by making the base plan extremely inviting and offering add-ons lightly. For instance, HDFC ERGO General Insurance’s recently launched Optima Secure Plus provides an attractive base plan with built-in features like Infinite Benefit, with 100% of base sum insured (SI) every year with no upper accumulation cap; Secure Benefit, which doubles the sum insured from the first day at no extra cost; and Unlimited Restore, where the base SI is fully restored after every claim, unlimited times in a year, among other features. “Even if the person is diagnosed with critical illnesses like cancer, his base SI will keep increasing without limit,” says insurance consultant Mayank Gosar.

Modular plans: Pros & cons

BENEFITS PAY for what you need. Reduced premium.

BUY a personalised plan as per health needs.

CUT out-of-pocket expenses by picking suitable riders.

AT renewal, opt for riders as per your life stage.

REDUCE waiting periods for specific illnesses.

DRAWBACKS TOO many riders can push up premium.

RIDERS may come with limits & co-pay clauses.

TO cut costs, you can end up being under-insured.

WITH age, riders may become too expensive.

CAN create confusion & complexity while buying.

Buy a modular plan if…

Benefits & drawbacks

Though modular plans offer high flexibility and are nominally priced, they require effort and diligence to go through all available options and choose as per one’s needs. It’s the personalisation of health insurance intended to simplify the purchase of complex health plans and to serve customers exactly what they need. However, is customisation truly helping policyholders or making things more complicated for them?

Cost-efficient: Most base plans are inexpensive, and though add-ons can increase the cost, it may still be a small price to pay for the convenience and flexibility of getting only the features you want. For instance, Niva Bupa’s Classic variant will cost `6,196 without any add-ons for a 30-year-old in Delhi, but increase to Rs.8,631 with three add-ons. “From the price perspective, modular plans are a valid way of keeping the premium low because the pre-packaged plans are becoming too expensive,” says Mahavir Chopra, Founder, Beshak.org.

“For instance, if you wanted to buy a Rs.25 lakh cover but it was not pocket-friendly for you, you didn’t have the option to downgrade, say, the room category, a couple of years ago. Now you can,” says Deshmukh.

Similarly, if you are 40 and don’t want maternity benefits in the plan, you don’t need to pay for it, or if you don’t want to pay for worldwide coverage or OPD benefits, you don’t have to.

High flexibility: You can not only pick and choose features at the time of purchase, but also alter add-ons at renewal as lifestage and medical conditions change. For instance, as a single person, you may not need maternity benefits, but when you get married, you can add this option during renewal. Similarly, as you age, you can add the OPD benefit or critical illness feature, which might be useful for lifestyle diseases after 40.

“At the time of renewal, policyholders should review whether the sum insured is still adequate, considering the lifestage developments across the year. At the same time, the alterations must be made only after a self-risk assessment so that it’s an accurate move towards being insured and not just having insurance,” says Saurabh Vijayvergia, Founder and CEO, Coversure.

Problem of plenty: While the choice and flexibility make modular plans attractive, they can also lead to confusion and over- or under-insurance for policyholders. “There’s a race on to provide all the best features, but it’s actually complicating the product further. There is no focus in terms of education and simplifying the processes after the policy is purchased, which may result in a wider trust deficit,” says Chopra.

Customers may not understand all the features and end up with either the ones they don’t need or leave out the ones they do require. “Typically, people don’t have the bandwidth to understand all the features and depend on others to help buy a plan. Hence, it will boil down to the person helping them sell the health plan,” adds Chopra. This could easily lead to overselling or misselling.

Visible add-ons: When you buy a health plan online, the add-ons that are offered to you depend on your personal inputs, often selected by artificial intelligence bots. Some of these can be pre-added to the base plan, with the option to remove or add more features. There’s a likelihood that you may miss out on some of the options and simply go with what is presented to you.

“Another problem is that most insurers file a large number of add-ons with the regulator, and file a document listing all of these. However, all these options may not be available if you are buying the plan online, which adds a layer of complication,” says Chopra.

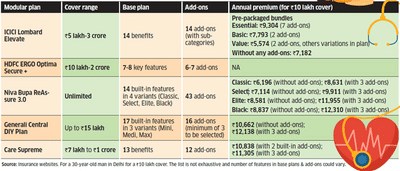

Some modular plans in the market

Who should opt for it?

The flexibility and convenience of modular plans benefits policyholders of all ages. “Customisation is for everyone because insurance was never designed to be a one-sizefits- all financial product. Each individual is different, so are their risks, and so should be their policies,” says Singhal.

However, buying a modular plan can be a cumbersome process for many, compared to purchasing a standard, pre-packaged plan. To make an optimal purchase, policyholders first need to understand the base plan, then review all the add-on features. Next, they need to calculate whether the price of each add-on and the overall cost fit their budgets, and finally check whether the selected add-ons are available.

If you want to make the most of modular plans, it’s best to be a handson buyer who can keep track of their changing insurance needs and carefully review the policy features while purchasing and at renewal. These plans may also work better for younger people with fewer needs or those with specific medical requirements.

What are modular plans?

A health plan consists of a base plan and riders or add-ons. Earlier, the base plan comprised fixed features that could not be changed, and one could add only 2-3 riders—usually critical illness, personal accident, co-pay/ deductible—at the time of purchasing the policy.

Over the past few years, the fixed base plan profile has altered and the number of optional features has increased to 15-25, each available at a price. These vary by insurers and can include a range of benefits, such as maternity, restoration of cover, reduced waiting periods for specific illnesses, inclusion of consumables, enhanced covers, hospitalisation daily cash, out-patient department (OPD) expenses and loyalty bonus, among several others.

Pre-packaged plans offer a solid base with a handful of riders; useful, but limited in scope. Modular plans flip this: a leaner base, and a far deeper optional layer. While pre-packaged plans are still available, more and more insurers are moving towards modular products.

Most insurers typically have a flagship modular plan that is highly customisable, while other plans in their portfolios are standard, with fewer customisable options. For instance, ICICI Lombard General Insurance has a modular flagship plan, Elevate, while others are being reworked. “The modular chassis has been built for the next generation retail product, Elevate, but the same approach has been applied to multiple product lines for the future, while the older, existing plans have been restocked by adding riders and add-ons,” says Priya Deshmukh, Head of Health Products, Operations & Services, ICICI Lombard General Insurance.

Most insurers keep basic features, such as in-patient, domiciliary, AYUSH (ayurveda, yoga and naturopathy, unani, siddha, and homoeopathy), and pre- and post-hospitalisations in the base plan, while specialised, ailment- or segment-specific and cost-saving features are kept as addons. “For instance, while there is a base plan that caters to family, there are womencentric covers that can be tagged to the plan as add-ons,” says Santosh Puri, Head, Retail, Underwriting, TATA AIG General Insurance.

“The practical goal is to plug the gaps a standard plan leaves, whether it’s outpatient expenses, consumables, or maternity costs, without paying for coverage that isn’t relevant,” says Singhal.

There are plenty of financial lures in both the base and optional features, such as enhanced covers, loyalty bonuses, reduction of waiting periods, etc. Take ICICI Lombard’s Elevate, which offers add-ons like Infinite Care, a one-time infinite claim; Power Booster, a cumulative loyalty bonus of 100% of the expiring or renewed annual sum insured, whichever is lower; Jumpstart, which reduces waiting period to 30 days for certain conditions; Claim Protector, for non-payables; and Inflation Protector to protect against inflation, among others.

Similarly, ReAssure 3.0 from Niva Bupa Health Insurance offers add-ons like Cash Bag+ (cashback on every claim-free year, among several other options); Niva Bupa One (exclusive membership); hospital daily cash; pre-existing disease wait time modification to 1-2 years; Wellconsult+ (up to five times the total premium for OPD coverage), among 43 such features.

Other insurers have tried to flip the pattern by making the base plan extremely inviting and offering add-ons lightly. For instance, HDFC ERGO General Insurance’s recently launched Optima Secure Plus provides an attractive base plan with built-in features like Infinite Benefit, with 100% of base sum insured (SI) every year with no upper accumulation cap; Secure Benefit, which doubles the sum insured from the first day at no extra cost; and Unlimited Restore, where the base SI is fully restored after every claim, unlimited times in a year, among other features. “Even if the person is diagnosed with critical illnesses like cancer, his base SI will keep increasing without limit,” says insurance consultant Mayank Gosar.

Modular plans: Pros & cons

BENEFITS PAY for what you need. Reduced premium.

BUY a personalised plan as per health needs.

CUT out-of-pocket expenses by picking suitable riders.

AT renewal, opt for riders as per your life stage.

REDUCE waiting periods for specific illnesses.

DRAWBACKS TOO many riders can push up premium.

RIDERS may come with limits & co-pay clauses.

WITH age, riders may become too expensive.

CAN create confusion & complexity while buying.

Buy a modular plan if…

- You understand the basics of health insurance.

- You are a proactive, hands-on buyer.

- You review insurance needs every 2-3 years.

- You are a new, young buyer, with simple insurance needs.

- You are willing to read the fine print, compare costs.

- You require specific medical benefits as per your health condition.

Benefits & drawbacks

Though modular plans offer high flexibility and are nominally priced, they require effort and diligence to go through all available options and choose as per one’s needs. It’s the personalisation of health insurance intended to simplify the purchase of complex health plans and to serve customers exactly what they need. However, is customisation truly helping policyholders or making things more complicated for them?

Cost-efficient: Most base plans are inexpensive, and though add-ons can increase the cost, it may still be a small price to pay for the convenience and flexibility of getting only the features you want. For instance, Niva Bupa’s Classic variant will cost `6,196 without any add-ons for a 30-year-old in Delhi, but increase to Rs.8,631 with three add-ons. “From the price perspective, modular plans are a valid way of keeping the premium low because the pre-packaged plans are becoming too expensive,” says Mahavir Chopra, Founder, Beshak.org.

“For instance, if you wanted to buy a Rs.25 lakh cover but it was not pocket-friendly for you, you didn’t have the option to downgrade, say, the room category, a couple of years ago. Now you can,” says Deshmukh.

Similarly, if you are 40 and don’t want maternity benefits in the plan, you don’t need to pay for it, or if you don’t want to pay for worldwide coverage or OPD benefits, you don’t have to.

High flexibility: You can not only pick and choose features at the time of purchase, but also alter add-ons at renewal as lifestage and medical conditions change. For instance, as a single person, you may not need maternity benefits, but when you get married, you can add this option during renewal. Similarly, as you age, you can add the OPD benefit or critical illness feature, which might be useful for lifestyle diseases after 40.

“At the time of renewal, policyholders should review whether the sum insured is still adequate, considering the lifestage developments across the year. At the same time, the alterations must be made only after a self-risk assessment so that it’s an accurate move towards being insured and not just having insurance,” says Saurabh Vijayvergia, Founder and CEO, Coversure.

Problem of plenty: While the choice and flexibility make modular plans attractive, they can also lead to confusion and over- or under-insurance for policyholders. “There’s a race on to provide all the best features, but it’s actually complicating the product further. There is no focus in terms of education and simplifying the processes after the policy is purchased, which may result in a wider trust deficit,” says Chopra.

Customers may not understand all the features and end up with either the ones they don’t need or leave out the ones they do require. “Typically, people don’t have the bandwidth to understand all the features and depend on others to help buy a plan. Hence, it will boil down to the person helping them sell the health plan,” adds Chopra. This could easily lead to overselling or misselling.

Visible add-ons: When you buy a health plan online, the add-ons that are offered to you depend on your personal inputs, often selected by artificial intelligence bots. Some of these can be pre-added to the base plan, with the option to remove or add more features. There’s a likelihood that you may miss out on some of the options and simply go with what is presented to you.

“Another problem is that most insurers file a large number of add-ons with the regulator, and file a document listing all of these. However, all these options may not be available if you are buying the plan online, which adds a layer of complication,” says Chopra.

Some modular plans in the market

Who should opt for it?

The flexibility and convenience of modular plans benefits policyholders of all ages. “Customisation is for everyone because insurance was never designed to be a one-sizefits- all financial product. Each individual is different, so are their risks, and so should be their policies,” says Singhal.

However, buying a modular plan can be a cumbersome process for many, compared to purchasing a standard, pre-packaged plan. To make an optimal purchase, policyholders first need to understand the base plan, then review all the add-on features. Next, they need to calculate whether the price of each add-on and the overall cost fit their budgets, and finally check whether the selected add-ons are available.

If you want to make the most of modular plans, it’s best to be a handson buyer who can keep track of their changing insurance needs and carefully review the policy features while purchasing and at renewal. These plans may also work better for younger people with fewer needs or those with specific medical requirements.

Next Story